Related Articles

In this first blog of Basics Of Income Tax we will talk on two topics:

- Standard Deduction

- Section 80

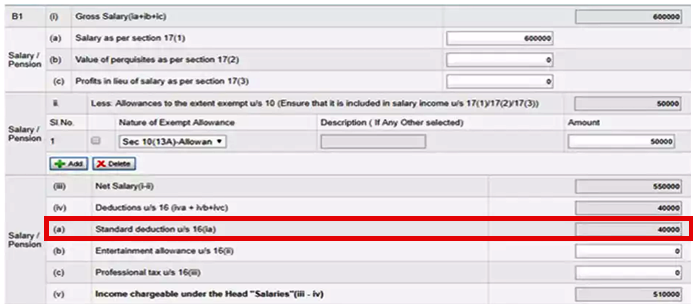

No matter in which tax bracket you are above two aspect certainly going to affect you’re of tax liability. Earlier Standard Deduction of Rs. 40,000 was done from gross salary, but from the FY 2019-20 it has increased to Rs. 50,000. Below is snapshot of place where you have to fill said amount for claiming standard deduction.

Now we move to very important & much complex topic of ITR filing Section 80. Section 80 constitutes of many sub section i.e 80C, 80CCC, 80D(1) & many more, this is the part of income tax filing which can be considered as gold mine for deduction seekers. The person who has understood this section can gain maximum benefit (deduction) & can save lots of hard earn money for self & family.

We will explain this Section 80 in 4 parts for better understanding, let’s begin with our first part on Sub Section 80C, 80CCC & 80CCD(1).

Sub Section 80C, 80CCC & 80CCD(1)

Many times we have heard from our friends & relatives that you can invest maximum of Rs. 1.5 L for getting rebate in income tax, this Rs. 1.5 L is invested in these three sub section’s only [Section 80C, 80CCC & 80CCD(1)]. Also our major investment (later we will learn more options of tax saving) taken place in these sub sections only (i.e. amount invested 80C + 80CCC + 80CCD(1) ≤ Rs 1.5 L). Let’s move further & discuss options available under these three sub sections:

Sub Section 80C : is most commonly used sub section for tax saving, most of our investment in done under this section only. Following opportunities are available under it:

- ELSS : (Equity Link Savings Schemes) these are type of mutual fund, usually come with lock in period of 3 years.

- Life Insurance : Term Plan & all other regular non annuity plan come under this sub section.

- Public Provident Fund.

- Senior Citizens savings scheme.

- ULIP’S : Unit Link Insurance Plan.

- Employee’s share of PF contribution.

- NSC : National Saving Certificates.

- Sukanya Samridhi Account.

- Five year deposit scheme (FD).

- Children’s Tuition Fee.

- Principal Repayment of home loan.

- Subscription to notified securities/notified deposits scheme.

- Contribution to notified Pension Fund set up by Mutual Fund or UTI.

- Home Loan scheme of the National Housing Bank.

- Deposit scheme of a public sector or company engaged in providing housing finance.

- Notified bonds of NABARD

Sub Section 80CCC : under this sub section you put your money in annuity schemes no matter whether it is of LIC or any other insurer. Annuity is amount received by person after some time at regular interval or immediately, so all those pension plan who come under above definition come under this sub section.

Sub Section 80CCD (1) : under this section employee’s contribution to NPS is considered for deduction. Those employees who have join Govt or PSU or PVT jobs after 2008 must be accustomed with National Pension Scheme (NPS). Every month a specific amount is deducted from our salaries for our NPS contribution, we can claim that amount for rebate under this section. Investment under Atal Pension Yojana (APY) can also be considered under this section. So above sub sections dealing with our major investment (i.e. Rs. 1.5 L) portfolio. But this is not all in our next blog we will talk about other sub sections & will further dwell in to possibility of saving more tax.